Blockchain: from technology approached with suspicion at its beginnings, when it was mainly associated with Bitcoin, to technology capable of giving an incredible acceleration to the processes of digital transformation in insurance carriers, whereby the advantages that blockchain can bring are so great as not to be taken lightly.

This topic was also addressed by BCG’s recent paper “The First Blockchain Insurer”, which calculates and quantifies what real benefits the whole industry could achieve already nowadays if blockchain technology were massively adopted. Specifically, the report mentions a reduction in the non-life combined ratio from 5 to 13 points, with an economic value in excess of 200 billion dollars in terms of technical margin from total gross premiums.

The first benefits will be greater efficiency and new services

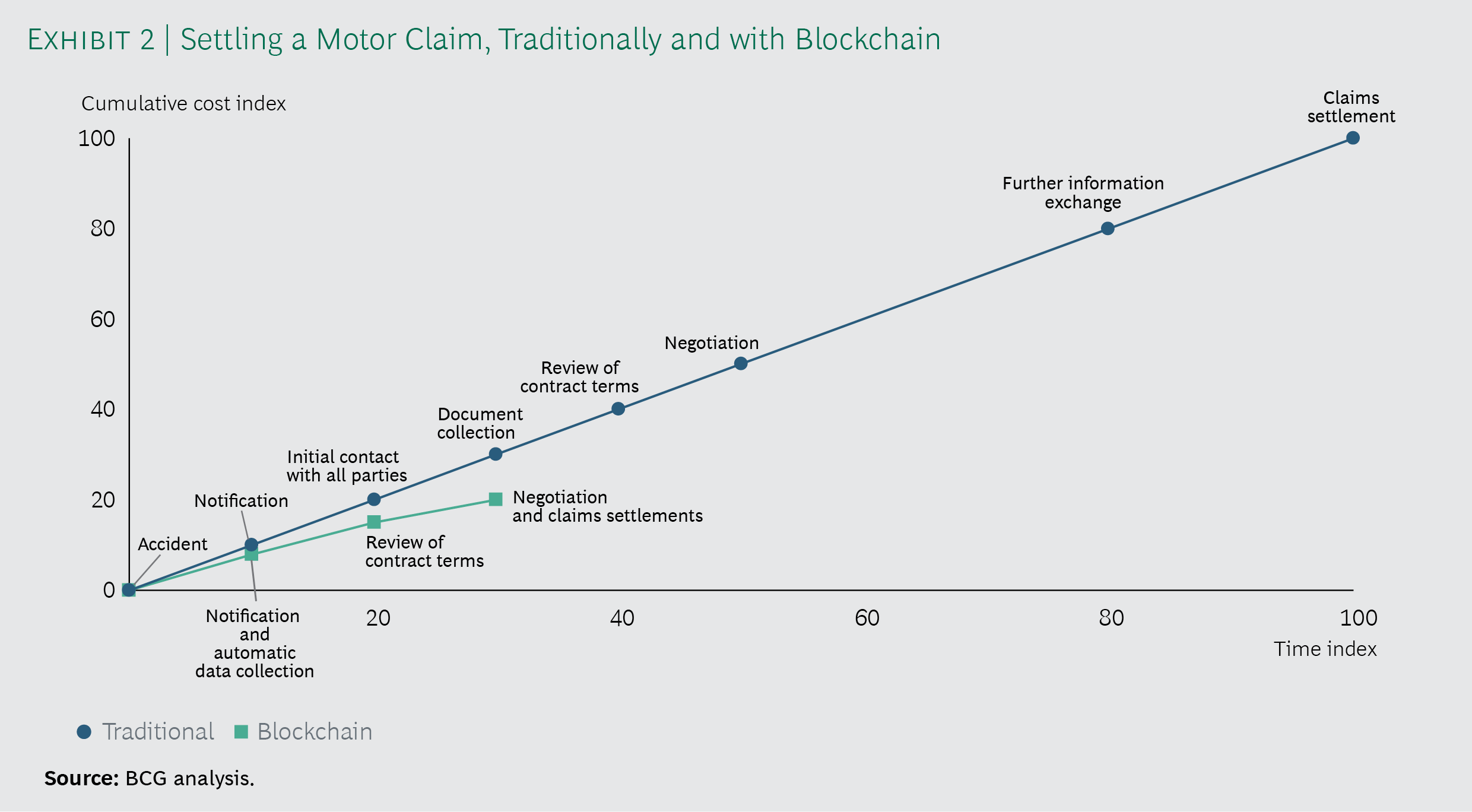

For BCG, a blockchain insurer can rely on greater efficiency in settlement processes throughout claims management with a significant reduction in costs and time needed to handle claims. The spirit of blockchain application to this industry is to be read in the transformation of the insurance industry value chain that reduces or eliminates the number of transactions thanks to the logic of Smart Contract. How?

Think about the case in which the risk of delay in a journey is covered by insurance. With blockchain it is no longer necessary to produce documentation certifying the actual delay of the service or fill in tons of forms for online damage assessment service. The certification of the delay comes automatically thanks to the reading of data relating to the services actually carried out for example by the airline company and again automatically triggers the procedure of compensation for the benefit of the insured. There are companies that already use the blockchain with their partners, but the real advantage may come when the ecosystem will use it, or when companies and third parties entitled to recover and certify the data can provide the data necessary for this type of management. The other big advantage of introducing blockchain in the insurance industry is the ability to securely access and manage Data Analytics solutions with predictive analysis. This approach allows on the one hand to reduce time and steps with savings in terms of management of the people involved. Other important benefits also come from the reduction of errors and fraud. Ultimately, the risk profiles of people can be defined much more precisely.

The Insurance-only blockchain model

Insurance companies may choose to work on a blockchain for their specific ecosystem of customers and partners, or may consider the possibility to create projects that fit into other existing ecosystems. The report highlights that today in the insurance world the choice that is defined insurance-only blockchain prevails with an ecosystem made up of different insurance companies and players in the institutional sector as associations or “Regulators” in a blockchain that allows the creation and sharing of data with a shared governance aiming to reduce costs, manual transactions, checks between different players involved in the same “practices”. This kind of blockchain can increase the awareness of all players both at KYC (know your customer) information level and at Risk Management level.

The Insurance ecosystem blockchain model

Some other insurance companies are choosing to follow the Insurance ecosystem blockchain model with an ecosystem concept that extends to other areas and allows access to other sources of information. In particular, this model makes it possible to develop forms of Risk Assessment based on the situation and context in which the services provided are set. The report gives the example of the logistics company, the “cargo company” Maersk, which is taking part in a strategic blockchain project in which the insurance and reinsurance company XL Group is also involved. In this situation, the accessible data are not only the conventional ones of the insurance industry, but also operational data, representing critical issues that may affect the business and may allow a more reliable management of risk assessment.

In both cases: Insurance-only blockchain and Insurance ecosystem blockchain, companies are addressing the possibility of implementing Smart Contracts to automate the most frequent and repetitive tasks with significant benefits in terms of resource management, time and dispute resolution costs.

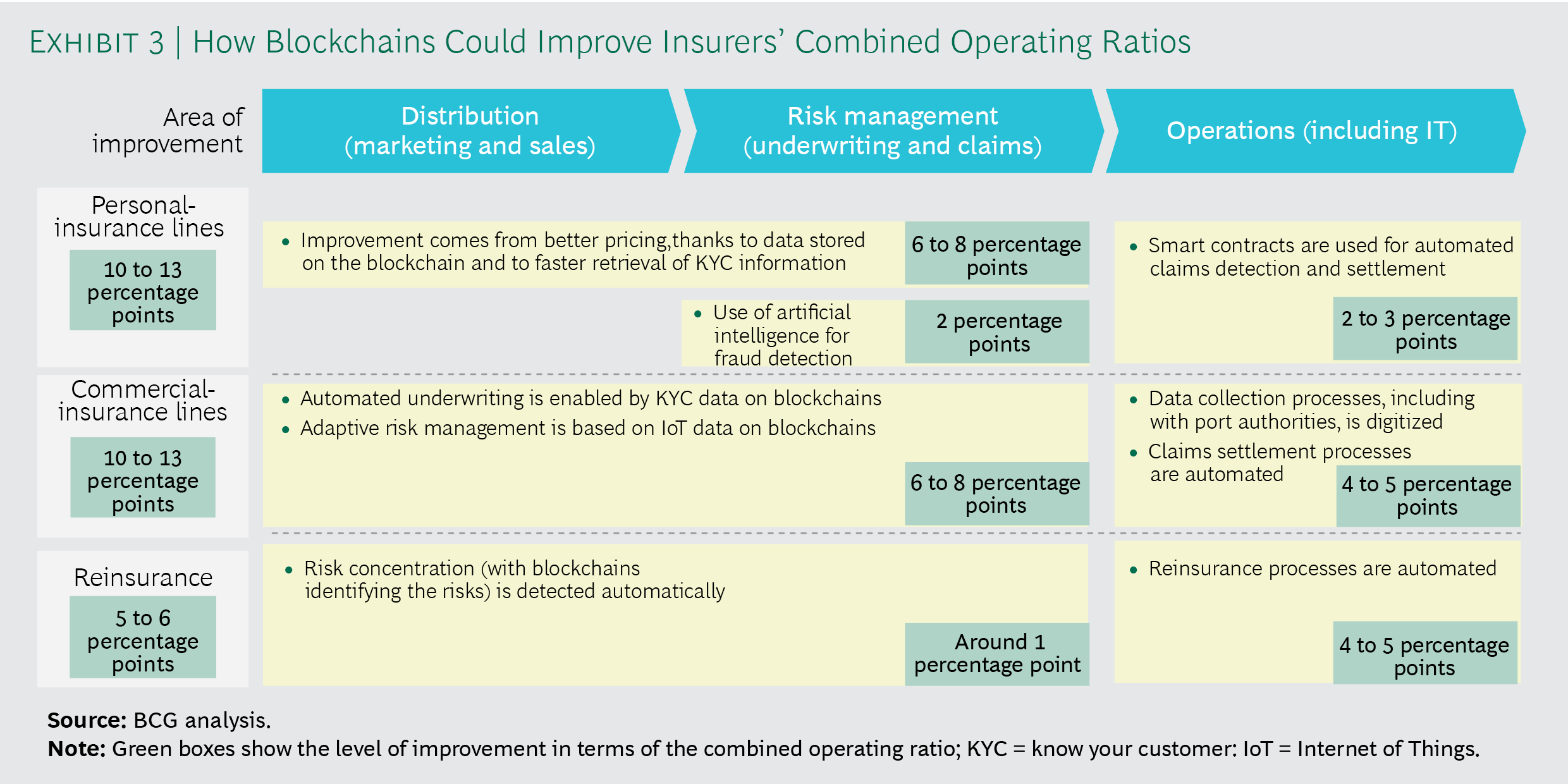

BCG mentions three large saving areas linked to the implementation of the blockchain:

- Distribution

- Risk Management

- Operations

In particular, the research highlights that the first examples of “All blockchain insurer” make it possible to achieve significant cost savings. In particular, in case of reinsurance services, the possibility of having data on a blockchain to be analyzed makes it possible to have a greater knowledge of risk concentration factors linked also to data from a socio-political or meteorological context or even from an environmental point of view. The fact that insured goods, for example, have to travel in areas of high instability or with a frequency of accidents linked to weather factors makes it possible to automate risk trading between companies and at the same time to manage costs more precisely. The research notes that, for example, the B3i consortium, which gathers dozens of reinsurance companies and brokers on a blockchain platform, has the prospect of reducing the loss ratio by 0.5% and the combined operating ratios by between 4 and 5 percentage points.

The BCG research then highlights the seven reference advantages of a blockchain-based choice:

- Asset tracking with maximum transparency

- Create reliable, unchangeable data sets

- Possibility of managing privacy and confidentiality with cryptographic solutions that allow to define data access rules only for blockchain participants

- Maximization of resilience thanks to the node structure these solutions are still active even in case of criticality on some nodes

- Possibility of achieving new efficiencies, with reductions in data management costs

- Automation of transactions with a different payment governance and contract management that allows a reduction of manual interventions

- Decrease of the time required for operations, transactions, and changes to data for all transaction elements

Blockchain, Internet of Things, data Analytics, Artificial intelligence

But the advantages of blockchain are tangible due to the integration of different technologies that contribute to innovation in the insurance industry, starting from the Internet of Things and advanced analytics, but also, and increasingly, solutions that combine Smart Contract and Artificial Intelligence. In compliance with the basic principles of insurance, which arise first and foremost from the collection of information, its selection and its retention. Such “information protection” model could be compromised by the blockchain that leads to the creation of value on other levels, i.e. the creation of an increasingly deeper and more precise knowledge that makes it possible to better manage all Risk Management and to carry out forms of prevention and forecast.

The advantages, as already mentioned, are huge. In particular, considering the automotive market, an insurance company that chooses to become “all blockchain” can aim to earn between 10 and 13 pps of operating combined ratio compared to a “conventional” situation. However, there is no shortage of risks and obstacles. The development of blockchain in the insurance sector is still hampered by the need to increase the skills and general know-how of the insurance sector. Then, absolutely strategic issues remain on the agenda, such as governance, on the one hand, and the lack of clear and recognized standards that require prudence in the choices made by operators, on the other. However, this cautiousness must be weighed against a market that finds new competitors in insurtech startups that are increasingly tough and, above all, natively prepared to handle these challenges, especially from a technological point of view.

All rights reserved