Over the last few years for Italian citizens dematerialization in insurance meant mainly one thing: the farewell to the insurance contrassegno [*] that every driver was obliged to display on the car’s windshield. Finally, thanks to an improvement of the IT systems for various institutions and companies, and to databases capable of communicating with each other, the Police may verify through the vehicle license plate if the latter is covered by insurance policy. A simple and effective Ania dossier (the main Italian association for insurers) explains the above and also indicates the reason why this system has been adopted: insurance contrassegno are easier to fake and the sale thereof is a widespread phenomenon in our country.

[*] The contrassegno is a little, pale yellow piece of paper inside the vehicle, at the windshield, in a special plastic “pocket”. This is the document certifying that a vehicle is insured for civil liability and is also in line with the payments and deadlines. In addition, the vehicle’s license plate number in such a counterfoil, is included so as to prove that the related motor vehicle insurance policy is linked to the vehicle on which the paper tag is displayed. It also contains the details of the insurance policy: the name and logo of the insurance carrier (and the details of the insured vehicle).

Widely encompassing the concept of dematerialisation in the insurance sector, we can see it includes many other things, in particular mobile and blockchain technologies.

Mobile dematerialization is already under way: all emerging insurtech startups (all of which are mobile first or mobile only) are “born” dematerialized. This means no scattering of cards: everything happens through the application, sometimes in a few clicks and within few seconds: choice of the policy, confirmation of the purchase, activation (by the insurer) of the policy and e-mail sending (or even by other channels such as facebook) of the contract, management of the claim.

Let’s take an example, recalling the case of the New York startup, Lemonade, as it offers plenty of food for thought.

In addition of being a peer-to-peer insurance carrier, “benefit corporation” certified, mobile first, applying artificial intelligence and behavioral economics, it’s also “100% paperless, zero paperwork”. Last January it got itself talked about for having resolved the compensation of an insured client in 3 seconds.

This shows how a fully digitized and automated process, with artificial intelligence technology working with data transparently and instantaneously, can reach amazing targets.

Dematerialization applies otherwise unreliable business models, for example in on-demand insurance policies, subscribed at the time of need, perhaps for a short lapse.

Let’s analyze Cuvva, a Scottish startup focused only on the car industry, compared to which it offers a service that many people have always dreamed of: a temporary car insurance policy, proportional with the actual and on-demand use. With a monthly subscription, ranging £ 10 to £ 30, depending on the car and the city you live in, it covers the risk of a “standing” car. When intends to use the car, the insured carries out a sort of “recharge” of the subscription, as from £ 1.20 per hour, only for the duration of driving, via the Cuvva app.

Even Neosurance, an Italian startup that has developed a technology for artificial intelligence companies, allows the sale of personalized micro-insurances through push notifications sent directly to the smartphone.

Such kind of models could never exist in a context based on “paper dictatorship”.

Dematerialization and mobile can also represent the sole opportunity to access services such as insurance in emerging markets, where citizens lack everything but definitely not mobile. The Swedish BIMA in this context built its own business, offering micro-insurance: the company enters into partnerships with mobile providers and insurance companies by connecting these two providers to deliver life, health and accident insurance via mobile phone. The rate is very low, integrated in the prepaid card, and the experience is seamless. Possible only in the age of dematerialization.

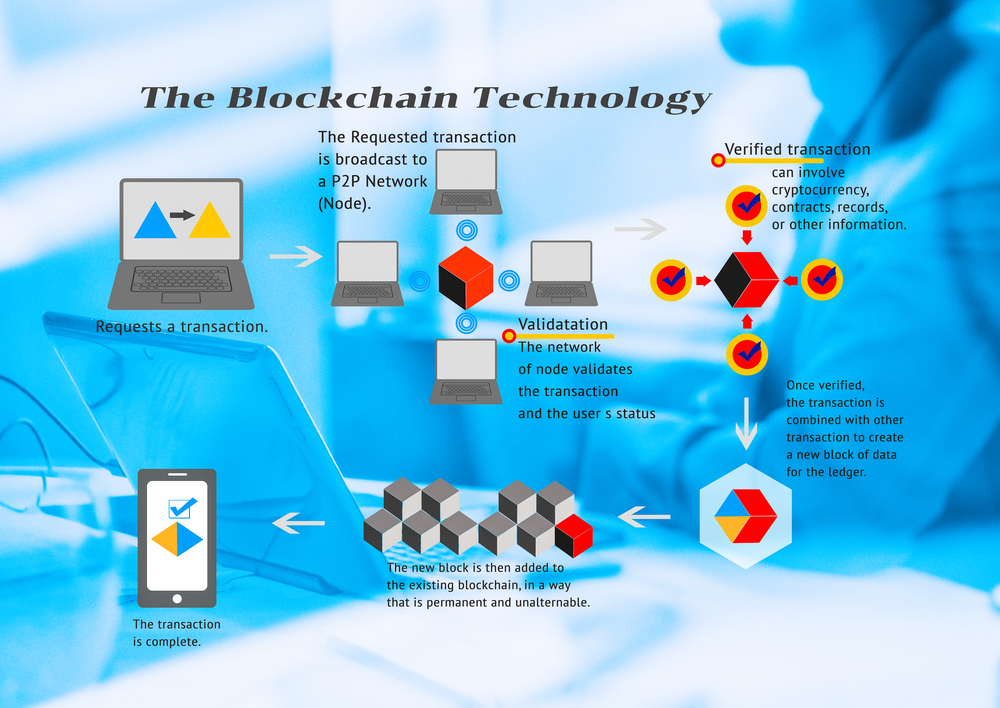

Let’s talk about the most extreme edge of dematerialization, blockchain technology.

Blockchain applications in red-tape contexts such as contracts, payments, identification of people or companies, administration etc. are so powerful that the banking sector and the insurance industry (but also large corporations and institutions ) are making several considerations.

There is a thing that the blockchain can do better than paper, getting mothball the Latin slogan “script manent, verba volant”: guarantee the information, its origin, its traceability. In short, it is a digital decentralization system, enabling a set of online transactions without the need for a central authority or an intermediary, giving the possibility to send, receive and store information in a “ledger”, a non-hackerable database as it is decentralized and disseminated, distributed among independent entities.

The power of the blockchain is the ability to support new financial transaction methods, improve existing insurance processes, and track (digital) documents. Blockchain-based digital currencies can support many new insurance models, in particular micro insurance and P2P. Many of the blockchain applications could be grouped into a new category of smart contracts: software developed and executed within a blockchain system. Since this technology is ironclad (and without human intervention), it is possible to develop and automate applications involving multiple players where the common concern is the trust.

With the smart contract, dematerialization reaches its peak, turning a contract into software.

There are many test and trials in this regard: Stratumn, Deloitte and Lemonway, the payment service provider, recently presented a blockchain-enabled solution known as LenderBot. This is a micro-insurance designed to protect the customers of services which fall within the concept of sharing economy. LenderBot allows people to subscribe customized micro-insurance policies, simply chatting through the Facebook Messenger App. The aim is to ensure high value products swapped round individuals, cancelling the intervention of a “super partes” supervisory authority in the insurance contract.

The Japanese insurance giant Tokio Marine & Fire Insurance Nichido, along with another IT giant, NTT Data Corporation, has instead launched blockchain technology trials to define trade policies, especially maritime ones.

Other trials are still progress in the Cat Bond sector, namely the one of derivatives issued by insurance carrier to share with other investors the risks associated with policies covering acts of God. An application field for blockchain technology already experienced by the Japanese Sompo Holdings and Allianz.

The level of dematerialization that the blockchain allows to reach is probably incomparable, even because this technology can raise protection against the cyber-risk intrinsic in the IT sector.

All rights reserved