Environmental changes, cyber risks, geopolitical conflicts, contagious diseases: these are some of the new risks mostly perceived by the global population. Risks very different from those of yesteryear which are creating a gap between what insurance companies have so far offered with their policies and the coverage that, however, consumers would prefer, both at personal and commercial level.

The World Insurance Report 2019, produced by Capgemini and Efma, has focused its annual research on ‘new risks’.

After having focused in past editions on the impact of digital transformation on insurance, this new report highlights how this digital transformation is the key for companies to meet new, complex needs, allowing them to conceive new policy and business models that can no longer be managed using traditional methods. Thus, the focus is back on the insurance product, which can only be technology-driven. However, the starting point (for companies) is the awareness of the need to face the issue of ‘new risks’ and solve it in an innovative way, which of course is also a great business opportunity.

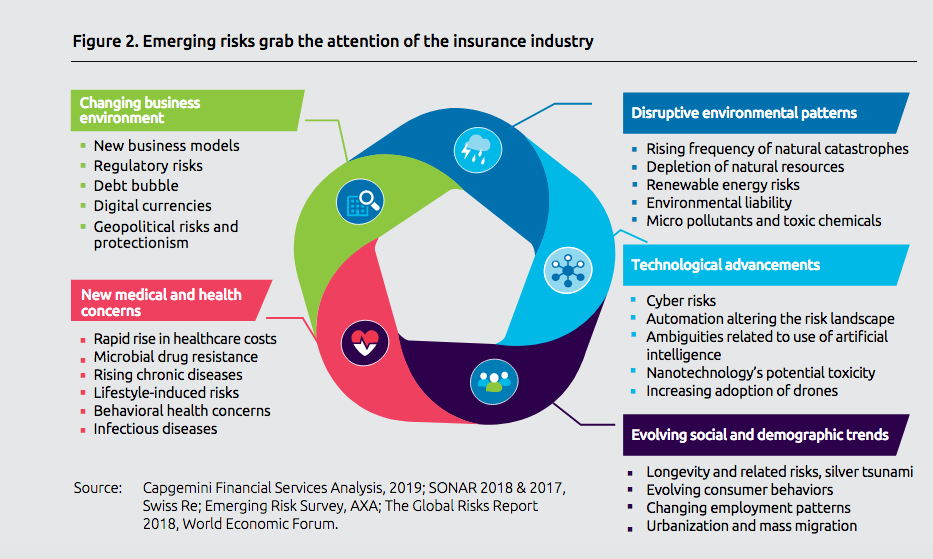

Many megatrends are affecting the risk profile, including climate change, new technologies, evolving social and demographic trends, new medical and health needs, an economic and business environment threatened by geopolitical turmoil (Just think about the US-China tariff “war”).

Such risk factors, identified with different priorities worldwide, can no longer be overlooked, affect life, health, property and business. For insurance companies, these are not only a responsibility consistent with their social mission, but also a great business opportunity. An opportunity so far little recognized by insurance companies, if, as the report suggests (compared to a survey carried out among 8000 insurance customers), people feel vulnerable and worried about not finding the insurance products they require. The changeover is not easy, requiring efforts both on the ‘cultural’ side ( to be focused on the customer) and on the technological, organizational and expertise side.

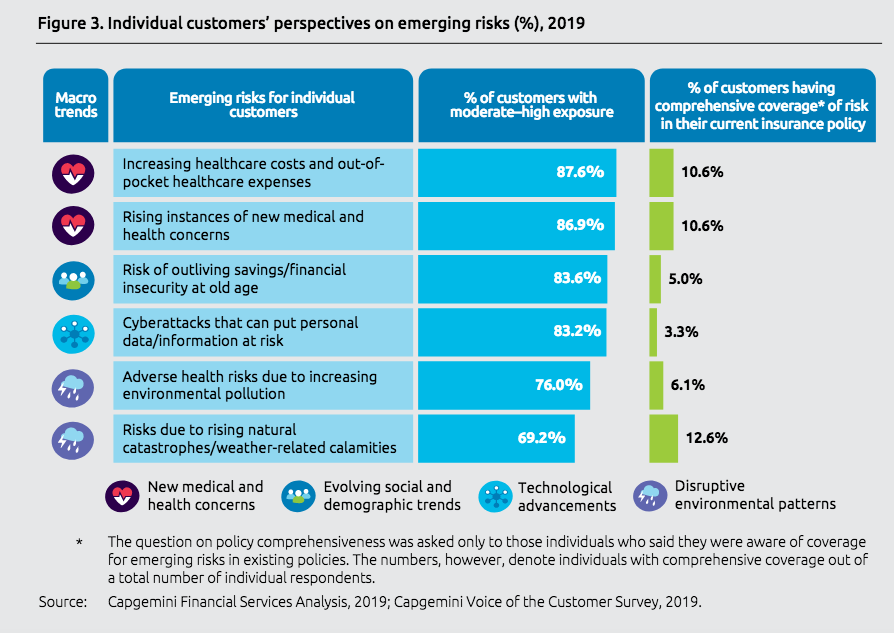

Health and medical risks are a key concern for people, while business customers report being concerned about the risks arising from business transformation; for both, cyber risk is a priority threat. Customer satisfaction is rather poor: less than a quarter of business customers and less than 15% of insured individuals feel to be fully insured against arising risks.

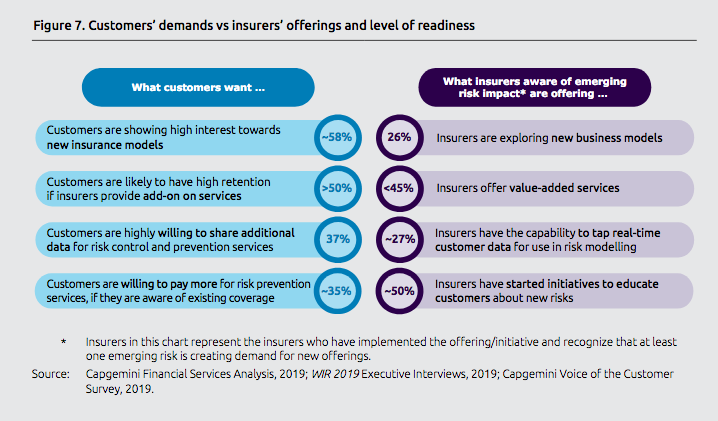

The report stated that insurance product pipelines are not in line with customers growing concerns about emerging risks, i.e. not yet consistent with the needs of the new risk outlook: 50% or less of the insurers surveyed (approximately 140 senior executives from all business lines in 23 markets) identified the impact of emerging risks in determining the demand for new offerings from customers and less than 40% of life and health insurers have developed a pipeline of new products to cover emerging risks in a consistent manner. More than 55% of customers are ready to scout for new insurance models, while only 26% of insurers are currently looking at such models.

A huge opportunity yet to be seized, despite customers being ready to share data and pay more to improve risk prevention services when a positive connection between risk exposure and insurance offering is perceived, where value-added, customised and flexible services are positively assessed, in particular by technology experts and corporations.

All rights reserved