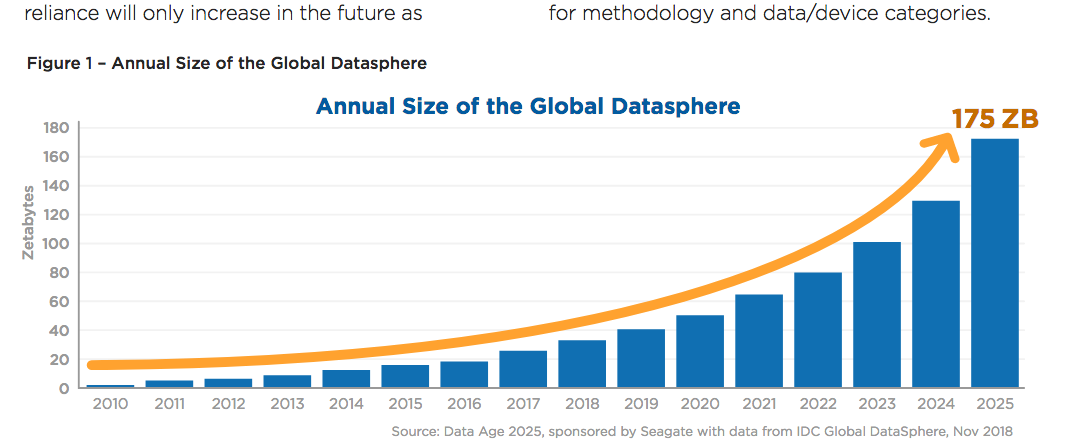

Big Data, in insurance, is a key element, which today faces several challenges, but presents enormous opportunities. The Companies have access to granular data like never before, each of us daily produces data, a huge amount of data, consciously (credit cards, social, apps, online searches, messaging, email, photos, videos, wearable); but also unconsciously, through digital medical records and administrative practices of various kinds digitized about us. Yet it’s not just people who generate data, but even companies, public and private organizations, connected objects, starting with our smartphones. The data is information in digital format and we generate so much of it that there is no really reliable estimate, they are all necessarily approximate. IDC in 2013 in a study for EMC predicted that in 2020 production will reach about 44 zettabytes worldwide, each person will generate 1.7 megabytes every second; but a more recent study (2018) of IDC for Seagate, even speaks of 175 ZB by 2025, more than 60 percent growth per year.

These numbers are impressive even when you do not fully grasp their size, but we can say that it is an exponential growth.

IDC takes an example to make you understand the size of 175 ZB (the entire Global Datasphere) and says: if you were able to store 175 ZB on DVD, then you would have a stack of DVDs that could take you to the moon 23 times or around the Earth 222 times.

Indice degli argomenti

Definition of big data

Big data are all information in digital format, they are huge volumes of data heterogeneous by source and format, which can be collected, stored and through special software analyzed, become knowledge and value.

According to most experts, big dates have certain characteristics. In 2001, Doug Laney, then Vice President and Service Director of Meta Group, described in a report the 3V Big Data Model: Volume, Speed and Variety. Today Laney’s paradigm has been enriched by the variables of Truthfulness and Value and for this reason we talk about 5V of Big Data.

What the “5V” of Big Data mean

Volume – Volume refers to the large amount of data generated every second. Data sets have become too large to be managed, archived and analyzed using traditional database technology, today distributed systems are used, where parts of the data are stored in different locations, networked and gathered by software.

Speed [Velocity] – Refers to the speed at which new data is generated and the speed at which the data moves. Just think of social media posts that go viral in minutes, the speed at which an email or message reaches its recipient or credit card transactions, the milliseconds needed for trading systems to analyze social media to gather signals that trigger decisions to buy or sell shares.

Variety – Refers to the different types of data we can use. In the past it was limited to structured data that could be included in tables or relational databases such as financial data (e.g. sales by product or region). Today most data is unstructured, i.e. heterogeneous – photos, video, audio, text, sensor or iot output, social media updates. With big data technologies today it is possible to exploit even this type of unstructured data and combine them with more traditional and structured data, to obtain ‘answers’, indications, forecasts, knowledge.

Veracity (Truthfulness) – Refers to both the confusion and reliability of the data. With unstructured data, quality and accuracy are less controllable, e.g. Twitter posts with hashtags, abbreviations, typos and conversational speech are sometimes unreliable. But volumes often compensate for the lack of quality and precision.

Value – Refers to our ability to extract from data analysis elements useful for improving business, service, our health, and any other context in which certain information can have a positive decision making impact. Many also define value as monetization, which is correct, but insufficient to understand the scope that data analysis can have in the quality of life and in different contexts where value is not only economic, but something different such as health, environmental sustainability, research, security, justice.

According to Bernard Marr (data expert and author of the book ‘Big Data – Using Smart Big Data, Analytics and Metrics To Make Better Decisions and Improve Performance) the V of Value is the only one that really matters. If data is not used, managed and understood, it does not turn into knowledge, which is ultimately what is needed to make more informed decisions, in business and beyond. From the customization of communication with the customer to the efficiency of production processes, passing through the management of flows and emergencies, Big Data Analytics have an impact in all processes.

The impact of Big Data

The use of data today is transforming the way we live and work, it is transforming our economies. Companies around the world use data to transform and become more agile, improve customer experience, introduce new business models and gain competitive advantage. Consumers live in an increasingly digital world, depending on online and mobile channels to connect with friends and family, access goods and services, and manage almost every aspect of their lives, even while sleeping. Much of today’s economy relies on data, even in an industry like agriculture, and this dependence will only increase in the future as companies capture, catalog and store data at every stage of their supply chain; businesses collect large amounts of customer data to provide greater levels of customization; and consumers integrate social media, entertainment, cloud storage, and real-time personalized services into their life streams. The consequence of this growing dependence on data will be a continuous expansion of the size of Global Datasphere.

On the business side, the sectors that can benefit most from big data are: Banks, Manufacturing, Telco and Media, Entertainment, Healthcare, Services, Retail/GDO, Utilities, Insurance, Agriculture, Marketing and Communication, Training, Education.

The only ‘obstacle’ to the use of data by the various industries, but in particular those that develop business with the end user, is the limits imposed by privacy and consumer protection issues, issues that must be resolved upstream with the intervention of the law that at European level has adopted, for example, the GDPR. But regulation is not the same all over the world.

Which Big Data in insurance: data enrichment

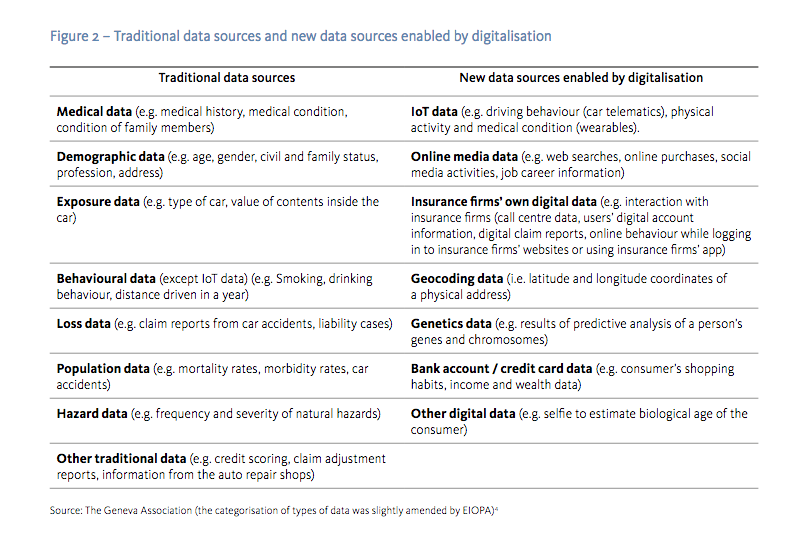

Insurance has always been an industry based on the use of data, necessary for a risk assessment, and the consequent setting of the premium, as accurate as possible. The processing of insurance data has traditionally involved demographic data, exposure data or behavioural data, but today, these traditional data sets are increasingly being combined with new types of data, such as Internet of Things (IoT) data, data coming from social networks and online behaviours, bank account and credit card data, in order to perform more sophisticated and comprehensive analysis, in a process commonly known as data enrichment. That through artificial intelligence and analytics, provide companies with the tool to revolutionize processes, operating costs, offers, customer relationship.

Big Data can help Companies in different ways:

– Risk assessment and premium setting. An example of an application in front of everyone’s eyes is in the field of car policies, where through the additional data provided by the black boxes it is now possible for Companies to reduce the premium, make discounts or even provide usage-based policies;

– Get to better know customers and their needs. Data analysis offers a deeper understanding of customer behavior, what they are looking for with insurance policies, potential problems that can cause friction, the most effective channels to reach them, and so on; this ultimately means improving customer acquisition, satisfaction and retention;

– Create new distribution models – virtual assistants, robot-consultants and chatbots improve customer interactions and make marketing more targeted;

– Innovate the business model. Big Data allows Companies to optimize and automate processes, reducing costs and improving effectiveness; but above all to act from a preventive insurance point of view, helping the client to prevent damage rather than dealing with mere compensation; to customize services and pricing, to create alternative models such as peer-to-peer, on-demand, micro policies, etc.;

– Claim management. Claims management is one of the areas that can benefit from Big Data, both in terms of customer experience and in terms of reducing fraud and operating costs.

Insurance companies are already using Big Data, but the situation varies slightly in the different branches.

For example, in Life and Health insurance, the use of new data sources (such as wearables) and data analytics software allows for the development of new insurance models that can not only be more targeted, but also encourage consumers to improve their lifestyle by offering discounts to those who perform more virtuous behaviors. However, in these areas the use of Big Data also raises questions about privacy protection, security and ethics.

The situation is simpler for non-life insurance, where such problems with data use pose fewer problems, as it is often encrypted data (GPS data used for car insurance, for example) or in any case less personal data, i.e. non-sensitive data.

One area where there is a wide application of Big Data and AI technologies is Travel Insurance. The relatively low price of the policy makes travel insurance a relatively quick decision and technologies can accelerate customer interaction, provide more personalized products and services, automate simple communication, improve customer satisfaction and quickly configure the most advantageous offer.

Big Data in Health sector

In the health sector, the data-driven approach radically changes the perspective of services and solutions also for insurance companies. Health is a primary good at every latitude and attention to this issue is entrusted to different public and private entities, in addition of course to the involvement of the person in the first person. The healthcare system is also very complex, traditionally plagued by problems of cost, efficiency and effectiveness.

Big Data technologies in Healthcare can lead to numerous benefits over all these typical, long-standing problems. But that’s not all, big dates finally make it possible to push and leverage prevention like never before. Insurance companies are also moving in this direction, reversing their traditional position of compensation in the event of illness towards support for disease prevention.

Thanks to the use of Big Data analytics and digital health monitoring systems (wearable, trackers, new generation medical devices, apps), insurance companies can now change their skin and play an active role in the health ecosystem, renewing their business models and customer proposition.

How Data Science evolves

Data Science is a cross-matter area applying scientific methods, processes, algorithms and systems to extract value from data. Data scientists combine expertise in various disciplines, including statistics, computing and business economics, to analyze data collected from the Web, smartphones, customers, sensors and other sources. Increasingly the data science team of companies will include humanistic profiles, such as psychologists, philosophers, anthropologists, behaviorists, as well as neuroscience experts.

Why?

It has now become clear that data collection and management cannot be a ‘wild west’, especially when it comes to personal and sensitive data: as we said at the beginning, each of us produces data every day, consciously or unconsciously. In this first decade of the ‘data economy’ boom, the limits imposed on privacy and data processing have been very few and big data have already revealed their dark side. Few concrete benefits for users. Europe pioneered standardised regulation with the GDPR, but in other countries around the world there are still no great limits. The State of California, the land of tech companies, has approved (it will be fully operational in 2020) a law inspired by the GDPR, the California Consumer Privacy Act. A strong step forward.

The law, however, with its timescales and its needs for the contemplation of different interests, will not keep pace with the exploitation of data and the continuous technological evolutions, it is therefore a good thing that the so-called ‘ethical approach’ is emerging, the ethical approach to data, which companies choose to make their own regardless of what the law would require.

The ethical approach to data requires companies transparency, fairness and a use that has as its ultimate goal the improvement of services in a customer-oriented perspective, able to return real value to the end customer. It is an important transition that brings a purely technical field, that of traditional Data Science, to integration with Human Sciences, which on the one hand help to understand and interpret the data themselves and make them more adherent to real life, also capturing emotional and irrational aspects; on the other hand they help to cultivate data ethics and support profitable but responsible business decisions.

All rights reserved